Cattle Report continues to show decreasing cattle inventory

The following is an article written by Dr. Kenny Burdine, Extension Professor, Livestock Marketing, University of Kentucky, and provides some good insight on what to expect from the cattle market for the rest of 2022.

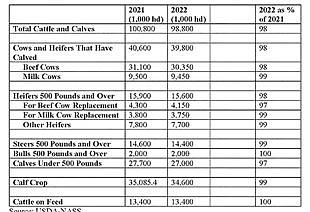

In late July, USDA-NASS released their mid-year estimates of US cattle inventory. As expected, the report showed lower inventory across most all cattle types. All cattle and calves were estimated to be down by just under 2%, while beef cow inventory was estimated down by 2.4%. This is very consistent with beef cow slaughter volumes, which have been running 14% higher than 2021. In nominal terms, 252 thousand more beef cows have been harvested through the first week of July this year than last year.

Much of this has been due to dry conditions in significant parts of cattle country, but high production costs and strong cull cow prices have also been factors.

Heifer retention estimates also paint a picture of a cowherd that is shrinking in size, which was estimated to be down by roughly 3.5%. In general, expansion occurs when heifer retention exceeds the long run average, while contraction occurs when heifer retention is below the long run average.

The retention has been about 1% below the long run average for the last four years.

One number from the report that looks strange at first glance is the cattle on feed estimate, which was actually flat from last year. Since calf crops have been getting smaller since 2018, one would expect on feed inventories to follow suit. However, consistent with decreases in heifer retention, more females are being placed on feed. Plus, dry weather in much of the country has pushed cattle into feedlots sooner than would have normally been expected. As we continue to see decreases in cattle inventory, these cattle on feed numbers are not sustainable and beef production levels will drop.

Since most cow-calf operations calve in the spring, most culling occurs in the fall, after spring-born calves are weaned. For that reason, the January inventory report tends to be a better measure of the size of the US cowherd. But, there is no doubt that 2022 is going to be another year of contraction for the US beef cow herd.

The combination high culling levels and decreased heifer retention are likely to result in something like a 3% reduction in the size of the US cow herd by January 2023.

Weather patterns, and prices for calves and cull cows this fall, will ultimately determine how many more cows leave the herd between now and the end of the year. A full summary of the July 1, 2022 inventory report can be seen in Table 1 below.

Exactly how continuing drought, reduced forage production and high feed prices will impact cattle and beef markets in the coming months remains uncertain. Nevertheless, the second half of 2022 is shaping up to look significantly different than the first half of the year.

Source:

Mid-year Cattle Report Continues to Show Decreasing Cattle Inventory, Dr. Kenny Burdine, Extension Professor, Livestock Marketing, University of Kentucky